Nobody likes talking about tax until there is a perk in there for them…Selfish right? Cue the Start-Up Tax Concession! (Not the sexiest name, we know.)

If you’re looking to issue shares or options to your employees through an Employee Share Option Plan (ESOP), it is worth considering whether you can do so under the ‘Start-up Tax Concession‘ (Concession).

Likewise, if your employer wants to grant you ownership in the Company, you should check if the Concession can apply.

Why bother with the startup concession?

In short, the Concession will make the offer for ownership in the employer company much more valuable for the recipients.

The ATO introduced the Concession in 2015. It was designed to make it easier for start-up companies to incentivse their employees with ownership in the Company. It also allows a simple way for the Company to use the options or shares as a way to ‘top-up’ a remuneration package, and ensure they can secure the right talent.

How does it change the tax treatment?

The Concession will allow the employee or contractor (Eligible Person) to only be taxed on the options received when they get a direct financial benefit. This means they won’t actually be taxed on the grant or exercise of options. Instead, they will be taxed when they dispose of them at a profit. For example, when they dispose of them by way of an IPO or acquisition, or by selling them back to the Company.

The Concession will also allow the Capital Gains Tax (CGT) discount to apply from the time the options are granted. For example, if an employee is granted options on 1 June 2020, and they don’t exercise those options (convert them into shares) until 1 June 2021, it will still be treated as though the employee has held the shares for the full 12 months to be eligible for the 50% CGT when they dispose of the shares.

The Concession also comes with less administrative burden – for example, employee annual reporting to the ATO is not required. However, minimal ESS reporting is still required for the company, in the year they grant the options.

What if the Start-up Concession doesn’t apply?

Outside of the Concession, the Eligible Person would generally be taxed on the discount value of the options or shares as if it is part of their annual income (this often occurs when they are exercised). This occurs despite the fact that there may not yet be any liquidity in those options or shares yet.

It is possible to set up schemes that defer this taxation, however these kinds of schemes require more specific criteria to be satisfied. These schemes will also have stricter compliance and reporting requirements.

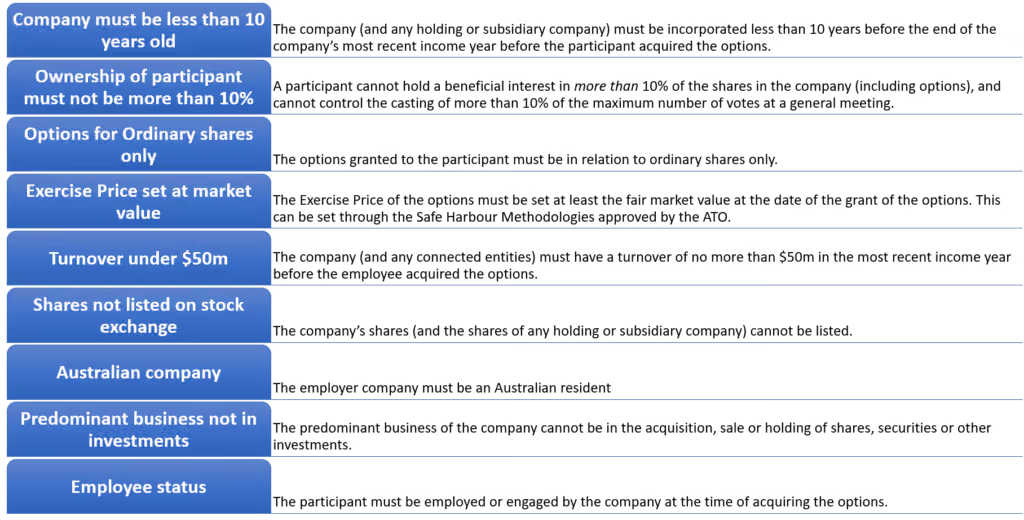

What are the eligibility requirements?

To complete an ESOP under the Concession, your Company needs to satisfy the following criteria:

Not sure if the Concession would work for you or your employer?

Want help deciding how to allocate your options or shares to employees?

Cake works with expert legal and accounting partners to check your eligibility and get your ESOP set up the most efficient way. Get in touch today!

This article is designed and intended to provide general information in summary form on general topics. The material may not apply to all jurisdictions. The contents do not constitute legal, financial or tax advice. The contents is not intended to be a substitute for such advice and should not be relied upon as such. If you would like to chat with a lawyer, please get in touch and we can introduce you to one of our very friendly legal partners.

.avif)